In the modern era of corporate finance, the balance sheet of a corporation has trended toward being less important relative to the income statement.

Back during Benjamin Graham’s quintessential value investing days, he looked at balance sheet valuation metrics almost as much as he did income-related valuation metrics. But in modern times, outside of certain circumstances, the balance sheet of an investment-grade company is treated as nearly irrelevant.

Profitable companies are expected to persistently decapitalize themselves by giving virtually all of their earnings back to shareholders, since in the era of ever-devaluing fiat currency, there has been nothing that they can hold on their balance sheet for long-term savings that isn’t dilutive.

This unfortunately heightens the risks for corporations over the long run by making them less able to navigate economic downturns or structural pivots when the need arises. By having nothing substantial saved up for a rainy day, they are constantly at the whim of capital markets, and are valued almost entirely on their forward earnings expectations which can fluctuate wildly.

Recent advancements can change this over time and will be discussed in this article, but first we can start by examining the existing options to see why they are so insufficient.

Corporations can hold cash or cash-equivalents such as T-bills, and indeed that is necessary in small amounts for working capital. But for longer-term savings, cash leaves a lot to be desired.

Beating the consumer price index is a false target. The fundamental question any saver, investor, or corporate treasurer has to ask themselves is, “am I getting diluted?” In other words, they need to know if their savings are becoming a smaller share of the whole system over time, and if so, at what rate?

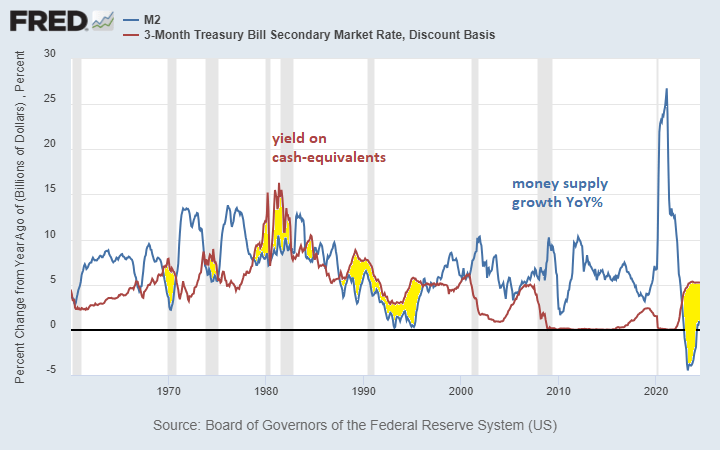

If you hold T-bills for a lengthy period of time as an individual or as a larger entity, your savings gradually become a smaller share of the dollar system over time.

In the United States, the money supply has historically grown by an average rate of about 7% per year. And across developed countries, that 6-8% long-term range tends to be typical. If you hold cash or cash-equivalents like T-bills and are earning an interest rate that is not keeping up with the growth rate of the money supply, then your share of the system is shrinking. You’re being diluted. In developing countries, the money supply growth rate is typically in the double digits.

There were rare periods like the 1980s through the mid-1990s where interest rates generally kept up with the money supply growth rate in the United States, but for the majority of the time, interest rates for bank accounts, money market accounts, and government bonds have all been substantially below the growth rate of the money supply:

St. Louis Fed

For simple numbers, if a company like Apple (AAPL) has $100 billion in cash savings, and the broad money supply is $20 trillion, then Apple’s share is 0.5% of all broad money. If they hold cash that yields 4% per year, then after five years they will have $121 billion. But if the money supply grew by 7% per year, then the money supply has grown to $28 trillion. They now only have 0.43% of the money supply.

After another five years, they’d have only 0.38% of the money supply. And five years later they’d only have 0.33%. And five years later (now twenty years in) they’d have only 0.28%. Their savings would be getting diluted away.

Of course, they can add new cash to their savings through income, but that’s like regularly adding more ice cubes to a melting stack of ice cubes. Ideally, they’d want to fix the storage situation of the ice cubes first, before adding more. Their savings are too entropic.

Put simply, cash returns fail to keep up with money supply growth, and are dwarfed by the rate of return that equity investors expect, which makes cash unsuitable for a long-term corporate savings asset beyond near-term liquidity needs.

Why Gold Doesn’t Work as Corporate Savings

Conceivably, a scarcer asset like gold could work as long-term corporate savings. But even gold gets diluted over time, albeit at a slower rate.

Professor Aswath Damodaran maintains records of the performance of various assets classes going back to 1928. For every $100 invested in T-bills in 1928 and compounded through 2023, an entity would have $2,249. Gold performed way better; $100 would have turned into $10,042 over that time period. Over the past century, every currency and every government bond has underperformed gold, inclusive of reinvested interest.

The problem is that an index of large stocks such as the S&P 500 turned $100 into $787,018 over that time, which dwarfed the performance of T-bills and gold. This is despite the fact that the majority of stocks underperform T-bills and underperform gold throughout their lifetime. The top-performing few percent of stocks outperform so dramatically that they lift the whole stock index up.

If a corporation wants to be a top-performing stock, they can’t hold large amounts of retained earnings in gold, since it has lower returns than what equity investors expect.

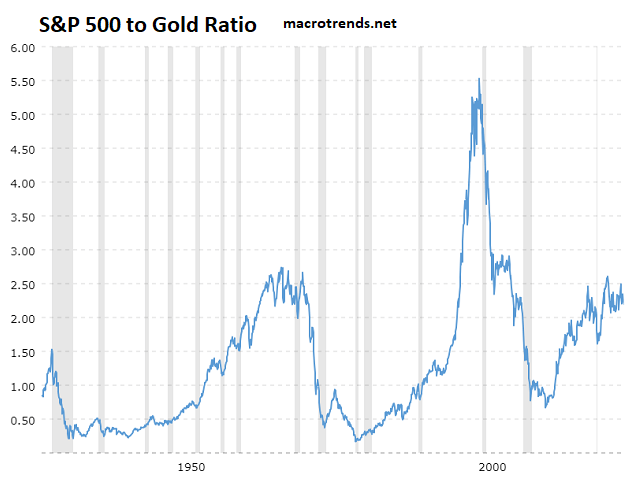

If we look at major stock indices like the S&P 500 relative to gold, on the surface, the performance differential doesn’t seem so bad. Stocks in aggregate don’t structurally go up vs gold, and instead tend to trade in more of a long-term range vs gold:

Macro Trends

But the total returns tell another story. The stocks in the S&P 500 paid dividends along the way. Those dividend yields normally ranged from 3-6% per year for most of the timeframe in that chart, and more recently have been 1-2% per year. Any investor who collected those dividends and reinvested them into more shares each year absolutely crushed the performance of gold by orders of magnitude cumulatively. That’s what makes holding gold untenable for a corporation.

And it’s in large part because of the gradual dilution that holders of gold experience.

From 1928 through 2023, to use the same period as Damodaran above, the U.S. broad money supply increased from approximately $54.8 billion to $20.8 trillion, which was a 380x increase. Gold’s price only went from $20.67 to $2,062, which was about a 100x increase. It failed to keep up with the growth of money supply by a factor of nearly four.

The global stock of refined gold increases about 1-2% per year. This means that during the 95 years included in this period, the total supply of refined gold increased by about 4x. The market capitalization of gold approximately kept pace with the U.S. money supply growth rate, but the price of individual units of gold did not, and the difference is approximately equal to gold’s cumulative dilution.

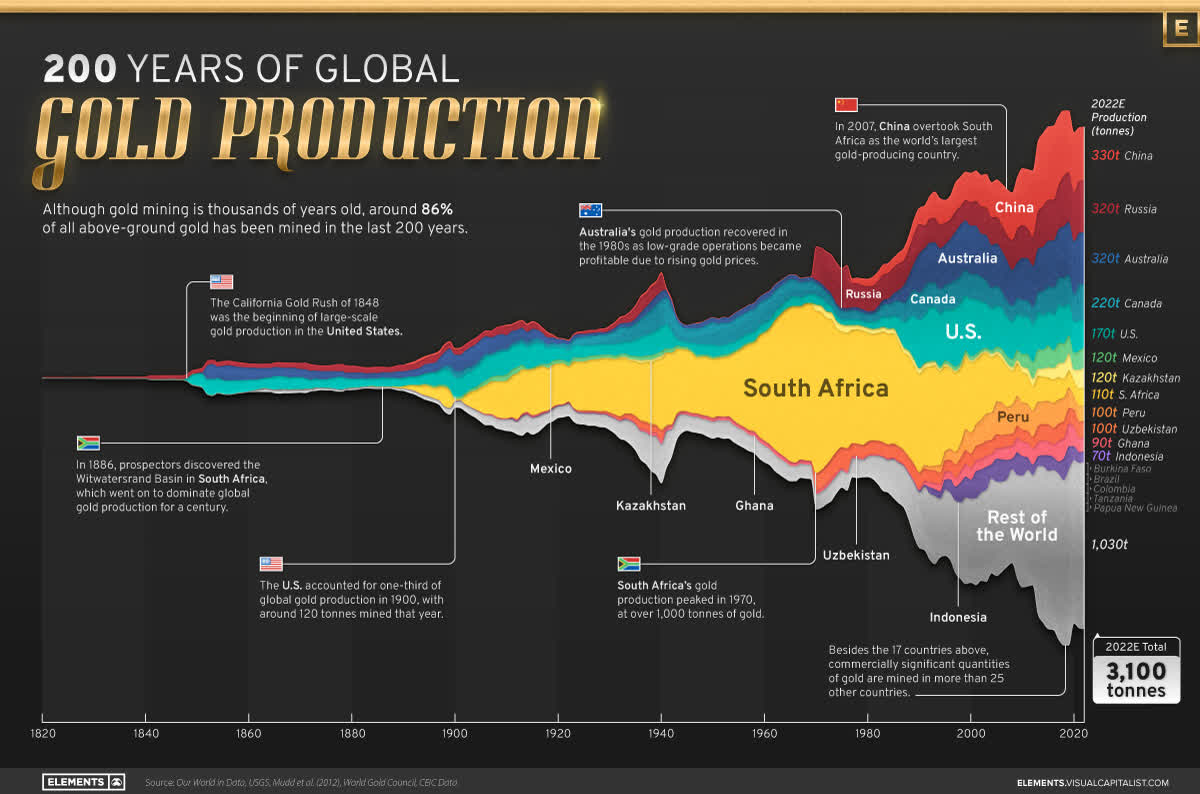

This chart from Visual Capitalist shows the estimated annual production of gold over time. We mine about six times as many tons per year as we did a century ago. This is a lot less exponential than the growth of fiat currency, but it limits the ability of gold to store value for an entity that is seeking to provide investors with top-performing equity returns.

Visual Capitalist

Putting it another way, if fiat money supply grows by about 7% per year, and the gold supply grows by about 2% per year, then the expected price appreciation of gold over the long run through periods of volatility would be about 5%, which is roughly what has occurred. That makes it a suboptimal store of value for corporations. Even gold miners usually don’t hold gold as savings.

Gold’s role, therefore,yea has not been to be a performant store of value, which is why we don’t find it on virtually any corporate balance sheets globally. Instead, it’s more of a pure defensive store of value, physically held by nation states and households in reserve for worst-case economic scenarios, or as a portfolio diversifier relative to bonds. Gold has been particularly useful as an accessible and reasonably liquid store of value in developing countries with less-performant stock markets and ever-devaluing currency, but it is lackluster when there are better options available and when you’re trying to keep up rather than merely play defense.

Why Other Assets Don’t Work Either

Other scarce assets like real estate and stocks have their limitations as savings assets for corporations as well.

They are more complicated and costly to manage and are outside of a corporation’s primary area of expertise, unless a company is specifically an insurance company or other type of large-scale investor. And by holding shares of the broad stock market, a corporation would technically be adding monetary energy to their competitors, which is not ideal.

Plus, most national stock markets don’t have the performance profile of United States’ equities. They don’t have the liquidity, diversification, or consistent performance that the S&P 500 has enjoyed. When we think about corporations, we should think about them globally, across multiple jurisdictions. Think of Canadian corporations, Brazilian corporations, French corporations, South African corporations, Japanese corporations, Egyptian corporations, and so forth.

So, if a company wants to build liquid savings in a way that doesn’t come with all sorts of complexity, that doesn’t add monetary energy to their competition, and that doesn’t require moving capital abroad to better performing equity markets, they have historically been out of luck. There have not been any great options, which is why they decapitalize themselves.

For example, both Coca-Cola (KO) and PepsiCo (PEP) have negative tangible equity. Their liabilities exceed their assets. Why do such successful and profitable companies run their treasury strategy like that? Because it’s better for them to be net short fiat currency, than to be net long fiat currency. And with their fairly consistent cash flows, they can get away with such a levered position. But many cyclical businesses have rather thin balance sheets as well, which can be quite dangerous.

The Risks of Corporate Decapitalization

In a world of only bad options for long-term liquid savings, corporations in aggregate have instead opted to return capital to shareholders. They decapitalize themselves.

Universities routinely build endowments which give them plenty of optionality to get through tough times, but the incentive structure for corporations has prevented them from doing this, and so the expected lifetime of a typical corporation tends to be far shorter than a typical university.

When a company has excess cash from operations, it has a few main options for what it can do with it:

Reinvestment: A corporation can reinvest into new business pursuits for organic growth, and that tends to come with the highest return profile when successful. But in practice, there are limits to what a corporation can successfully do on this front over any given period of time, without venturing outside of their core area of expertise.

Acquisitions: A corporation can acquire some other entity. This can make sense at times, but it comes with all sorts of risks. For example, there is integration risk; company cultures may clash and be dilutive to the acquiring corporation. The corporation may become bloated and unfocused. Pursuing unnecessary acquisitions is a common form of malinvestment.

Savings: A corporation can save the cash, but as previously described, this is dilutive. Corporations are heavily incentivized to not have substantial savings, since anything they could easily save in has a return profile that is lower than their cost of equity capital.

Dividends: A corporation can pay dividends to shareholders. It does make sense for a company to pay its owners, after all. But problems can arise if they pay all of their savings out, which they often do because they have no strong method to save value in.

Buybacks: A corporation can buy back its own stock, thereby increasing the earnings per share and dividends per share. It’s mechanically similar to paying dividends, except the “dividend” in this case is in the form of more equity ownership per share owned, rather than cash.

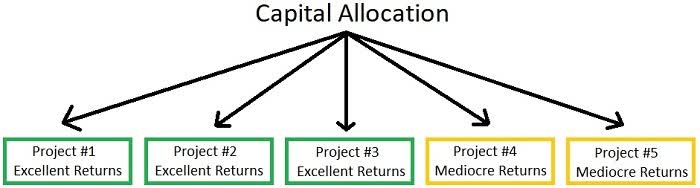

Back in 2017, I wrote an article about why corporations that persistently pay dividends (or perform buybacks) tend to outperform those that do not. Ultimately it comes down to capital discipline rather than the dividends themselves. If a company has excess cash and there are no good savings assets for it, what you don’t want them to do from the perspective of a shareholder is to invest it into anything and everything. You’d rather have them just invest in their best ideas, and then return the remaining capital to you so that you can either spend it elsewhere or reinvest it back into their best ideas. Here’s the key snippet from that 2017 article:

In any given year, a company has a certain amount of money that it can invest into various projects. These could include internal growth opportunities like launching a new product or building a new store, or it could involve acquiring another company.

Of course, not all of those projects will be equal. Some of them are excellent opportunities within the company’s core competency that are likely to generate excellent returns on capital, while other ones are more mediocre/borderline opportunities.

And a company has a limited amount of money to invest at any given time. Ideally, they want to invest in the best projects to generate the best rate of return for shareholders. If they invest in bad ideas that lose money, it destroys capital.

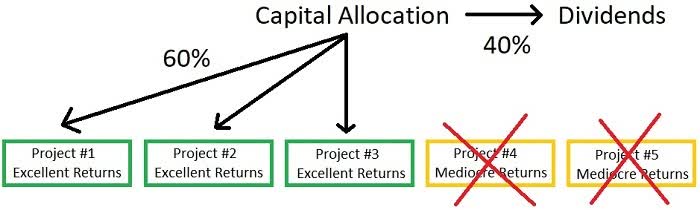

For an undisciplined company that is big enough that it should be paying dividends but isn’t, this graphic shows how they generally spend their money:

Lyn Alden

If they have enough money lying around, they have more liberty to just throw money at all the potential projects, even mediocre ones. A “project” in this sense could be an internal growth opportunity like a new product or new store, or it could be an acquisition.

Tech stocks that don’t pay dividends are infamous for making overvalued acquisitions- they buy companies that don’t even make a profit yet for billions of dollars, like throwing darts at a dartboard to see what sticks. Ten years later you can look back and ask, “what value did they ever get from that?”

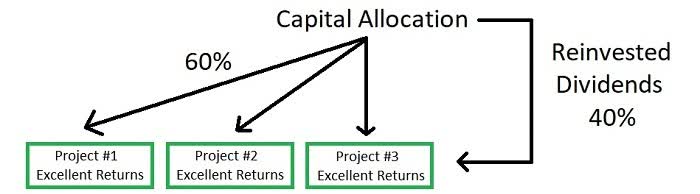

However, suppose that a company has a disciplined capital allocation policy, and they pay dividends to shareholders every quarter, and grow those dividends every year. This leaves them with less capital to invest, and therefore they need to be more selective in terms of which projects they invest in.

Their example would look more like this:

Lyn Alden

They don’t have tons of cash to liberally just invest in everything, so they invest in their best ideas relating to their core business, and give the remaining funds to shareholders as dividends or buybacks.

Those investors can spend those dividends as income or they can reinvest those dividends into buying more shares of the company. That way, you keep compounding exponentially in the company’s best projects with 100% of the capital.

Lyn Alden

Individual dividends aren’t magic. When a company pays a dividend, its stock price goes down slightly in the short term to adjust for the fact that some cash has left the company.

But what separates excellent companies from mediocre companies over the course of decades is that excellent companies produce better returns on invested capital, which I will cover in the next section. And as an investor, it’s better to have a company that is disciplined and selective with its projects and returns excess capital to you than a company that simply invests in all potential projects.

In a world with no savings assets that are good enough to be on a corporation’s balance sheet and keep up with the cost of equity capital, that makes sense.

But especially for technology businesses or cyclical businesses, when a corporation sends virtually all of its earnings back to shareholders, it builds no “rainy day” fund. If the company is ever in need of capital to get through a problem or to pivot toward a big new investment, it will be entirely reliant on current market conditions to get financing.

And as a decapitalized entity, its market valuation will be entirely reliant on its earnings prospects, since it has little value on its balance sheet. A corporation that has decapitalized itself can easily find itself in a situation where some problem has impaired its future earnings potential, which also impairs its valuation and ability to raise capital at the same time. If they had a substantial amount of stored-up capital, then they’d have some of their own internal options to deal with the problem that don’t rely on the fickle generosity of external investors and current market conditions. And how much stored-up capital that a corporation requires might vary depend on how cyclical or disrupt-able they are.

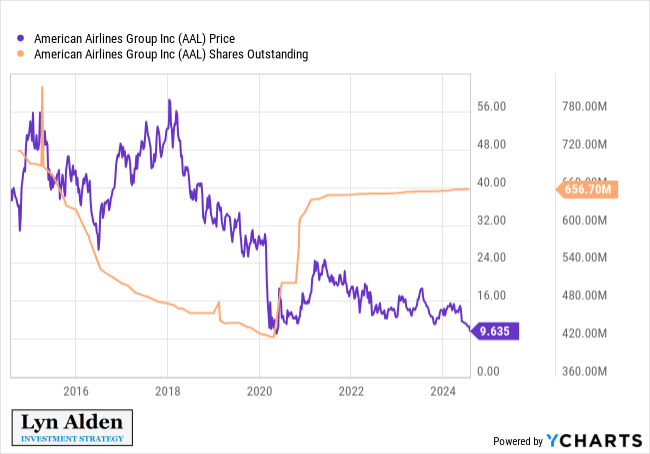

An easy example to point to is what happened to airline corporations during the pandemic in 2020. In the decade prior, most of them had returned virtually all of their earnings to shareholders, since there was no good non-dilutive savings asset for them to hold. But then when they were struck by a sudden environment of drastically reduced air travel, they had no savings to get through it.

So in the United States and a number of other countries, airlines were collectively given tens of billions of dollars of bailout money, and some of them also had to issue a lot of new shares at low prices to raise money from capital markets. In other words, they had to take equity-dilutive actions to recapitalize themselves at exactly the wrong time for shareholders.

This wasn’t good for either taxpayers or shareholders, and it occurred in large part because corporations like them are penalized for holding any savings:

YCharts

Let’s consider two hypothetical companies to further illustrate this.

Example 1: Decapitalized Business Crisis Scenario

The first company doesn’t have much savings. It has working capital and some illiquid property and equipment, offset by payables and some debts, so their balance sheet equity is negligible. They earn $1 billion in net income per year and trade at 20x earnings, so they have a market capitalization of $20 billion.

But one day they run into very bad news. Maybe it’s a pandemic that hurts their revenue, or maybe it’s a severe recession, or maybe they just lost their biggest customer to a competitor and some of their key investors begin to doubt their competitive advantage. Their net income drops to $500 million.

They are short on cash relative to the investments that they believe they need to make to get back to structural growth. They turn to stock and bond investors to raise capital, but they find themselves with unattractive options. For debt, the available terms from bond investors are rather high-yielding now. For equity, they find that the market is now only willing to pay 10x earnings due to their lack of growth, which on $500 million in net income is only a $5 billion market capitalization. If they issue shares to raise capital, they’d be doing it with four times as much dilution for shareholders as they could back when their market capitalization was $20 billion. Bond investors and stock investors mostly just have to rely on the company’s forward earnings potential when judging the value of an investment, since it doesn’t have much of a balance sheet to speak of. This puts the company in a rough spot, and subject to the whims of the market.

Example 2: Capitalized Business Crisis Scenario

The second company has five years’ worth of income as accumulated savings, or $5 billion in net savings. They earn $1 billion in net income per year and trade at 20x earnings plus their savings position, so they have a market capitalization of $25 billion. And like the other company in this scenario, we can imagine that they run into a period of turbulence where their income drops to $500 million and they need to make some key investments for growth or mitigation.

Unlike the first company, this company doesn’t need to issue expensive debt or dilutive equity at the wrong time. They can just tap into their savings, with zero equity dilution. And if they do want to issue debt for some financing, it would likely be lower-yielding debt, because bond investors would be more assured of getting their money back due to how much savings the company has.

Both stock investors and bond investors in this scenario, to the extent that the corporation even needs them, are not evaluating the company entirely for its earnings prospects. Instead, the substantial balance sheet helps to dampen the company’s volatility in terms of its market capitalization, since even if their earnings were cut in half, their balance sheet is still there and that’s a significant component of the total valuation.

Can Bitcoin Fix This?

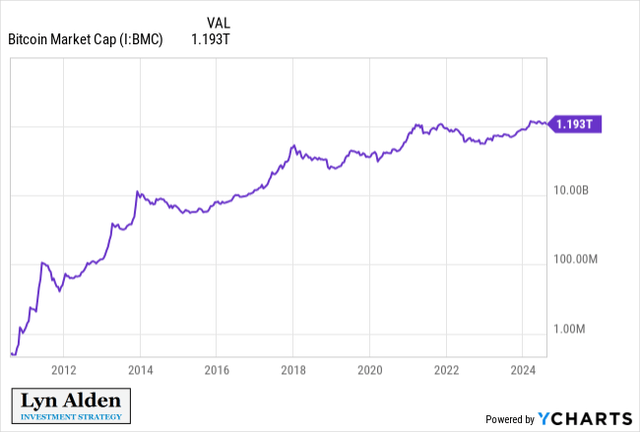

Bitcoin (BTC-USD) is a powerful savings asset because unlike gold, it has zero long-term dilution. The supply cap is 21 million, which is enforced by the distributed node network. And it has been the best-performing asset for quite a while:

YCharts

If an entity holds cash-equivalents, gold, or other liquid savings assets, they get diluted over time, endlessly. With bitcoin, there is zero dilution over the long run. Coins are issued at a declining rate until they reach a supply cap of 21 million, and by the mid-2030s over 99% of coins will have been mined and put into circulation. As of this writing, nearly 94% of coins are already mined and in circulation.

That seemingly small difference in dilution between bitcoin and gold is bigger than it seems. Over the long run, gold underperforms major equity indices by an amount that’s roughly in line with its 2% annual dilution rate, but that rather small performance gap is what makes it unattractive for a corporation to hold, since it underperforms the rate of return that equity investors want. Having an asset with no dilution, and that therefore can potentially keep up with major equity indices, suddenly makes corporate saving a serious possibility. Crossing that small gap is a zero-to-one moment for corporate savings.

And if a corporation holds stocks or real estate, it comes with time and complexity to manage. Real estate is not very liquid. Stocks are liquid, but investing in them gives monetary energy to competitors, and might even entail investing offshore and giving monetary energy to other nations.

Bitcoin is potentially the fix for this. It’s faster than fiat currency, and harder than gold. It’s liquid, and it’s easy to hold.

However, the Bitcoin network is only about 15 years old. For the first decade of its existence, it was not at any sort of institutional scale in terms of size or liquidity, and had all sorts of regulatory uncertainty. It was basically a science experiment from the perspective of any large capital allocator.

And volatility has been a major issue, and will continue to be for some time as long as it’s still going through its exploration and adoption phase and reaches greater levels of distribution. It’s not at a steady-state yet, in other words. It hasn’t reached its total addressable market. It’s more of an emerging store of value than a stable one, at this stage. And in the meantime, this volatility impairs bitcoin as a savings asset for a timeframe of a few years or less. It’s only a useful savings asset for 4+ year increments, and preferably longer. Not knowing the purchasing power of your savings when you might need to spend them, is similar to potentially having to issue dilutive equity at bad prices.

At this point, however, Bitcoin’s network effect dominance has become pretty clear, the scale in terms of size and liquidity has reached an institutional level, and various regulatory uncertainties and accounting treatments have improved.

When we look at the history of protocols, whether it’s Ethernet, File Transfer Protocol, Internet Protocol, Simple Mail Transfer Protocol, Universal Serial Bus, or others, 15 years tends to be enough to prove themselves. In the early stage of a new field of development, young protocols tend to compete with each other. But eventually one of them achieves network effect escape velocity, and at that point has a very long and potentially indefinite expected lifetime. Bitcoin is a monetary protocol.

Bitcoin has been the largest cryptocurrency by market capitalization for 15 years straight, is purposely simple and robust on the base layer like most successful protocols are, and has likely reached that point of network effect escape velocity as the dominant protocol of value. That’s not to say that it’s without risk, but the risk profile keeps shrinking over time.

At this stage, early adopters do take on price volatility and tail risk, but that comes with bigger potential returns than what will be the case for later adopters. In another 15 years, it may very well be the case that the Bitcoin network is far larger than it is now, with more holders, more liquidity, less volatility, and a lower return profile that is still a very strong one for corporate savings.

Many small businesses hold bitcoin on their balance sheet. It’s generally easier for small companies to take decisive action, because only one or a few people have to make key decisions. Larger corporations generally have a lot more stakeholders and checkpoints involved, which reduces risks but slows down decisive action. It takes time.

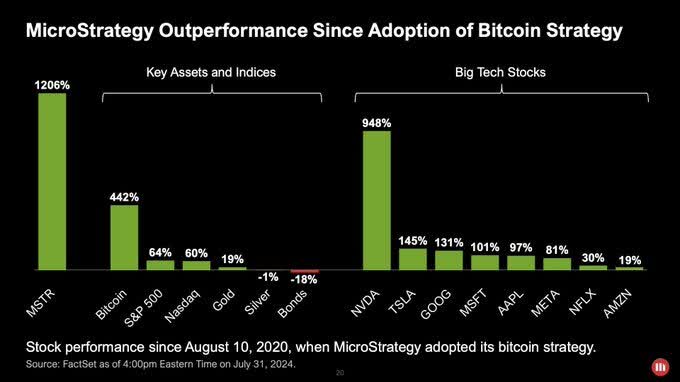

But some larger companies have already adopted it as well. The most famous example is MicroStrategy (MSTR), which began converting their corporate treasury to bitcoin in August of 2020. That was four years ago this month. They’ve enjoyed massive outperformance since then in terms of share price and total enterprise value.

MicroStrategy

Other public companies, ranging from Tesla (TSLA) to Block (SQ) to Alliance Resource Partners (ARLP) to Semler Scientific (SMLR) to Metaplanet (TYO: 3350) have also put part of their corporate treasury into bitcoin. New FASB rules for crypto assets are making this easier to do. Bitcoin Treasuries maintains a large list of entities that are known to hold bitcoin.

A key way that many of these companies manage the volatility and risk is by only putting a portion of their savings in. This limits their total volatility and tail risk, while still benefitting from building corporate savings. For the money that they are virtually sure they won’t need for 4+ years, they can put it in bitcoin. It doesn’t have to be all or nothing; a company can reinvest some capital into good growth projects, can return some capital as dividends or buybacks, and can build a long-term savings base with bitcoin.

Some small nation states have done it as well. The country of El Salvador, in addition to making bitcoin legal tender, holds a portion of their sovereign reserves in bitcoin. The Kingdom of Bhutan has been mining and holding bitcoin for years.

Other entities have run into landmines. The most common landmine has been to buy a lot of crypto company equity rather than bitcoin itself. Large pensions and sovereign wealth funds bought FTX equity, for example, thinking that this was a safer asset than bitcoin. Equity is a well-known asset class to them, and they felt more comfortable with it. But ultimately, that wasn’t the way to go, and it still isn’t. Simply owning bitcoin over the long run is the base asset that outperforms most complex schemes within the industry, and so it makes sense to own bitcoin first before considering other options.

For the next several years, bitcoin’s price volatility will likely continue to be high, and the rate of corporate adoption for bitcoin as a savings asset is difficult to predict. As of this writing, it’s still mostly for executives with high volatility tolerance and a willingness to be wrong for quarters in a row.

But if we fast-forward to Bitcoin at year 30, if it indeed continues its trajectory of growth and adoption and gradually lower volatility, then it could seriously change the nature of corporate finance. In that world, a corporation will be able make more use of its balance sheet, and it will be able to build in some protection against cyclicality and trend changes rather than be effectively forced to decapitalize itself and remain at the whim of market conditions. In other words, corporations could normalize having “endowments” in a similar way that universities do.

In the meantime, I tend to be bullish on early adopters relative to their peers. I’ve owned MicroStrategy in my portfolio since they adopted their strategy four years ago, and I will continue to look for entities that pursue a similar strategy. Companies that (at least around the margins) seek to store some of their retained earnings in bitcoin will continue to be on my watch list as potential outperformers.

The Best Candidates

The biggest and fastest-growing companies are unlikely to be first movers on this. They have less incentive to be.

The best candidates for being early are actually the stagnant companies. Publicly-traded “value stocks” that are profitable but have only modest growth prospects, can gain a lot from this strategy, especially if they are early to it. Rather than constantly decapitalizing themselves and chugging along as an underperforming stock, they have the option to do some shock therapy, and truly change course. There are hundreds of stocks like this throughout the U.S. stock market, and thousands globally.

They can begin building a war chest of savings in an asset that, in addition to being absolutely scarce, has been undergoing a structural adoption phase for fifteen years and counting, and thus is growing at a faster rate than most other assets over any given four-year period. It’s volatile, which is why the existing winners (mega-cap outperformers) are less likely to consider it.

And at this stage, the strategy can excite certain stock and bond investors. Metaplanet (TYO: 3350) is up over 3x since it initiated its bitcoin treasury strategy in April of this year.

In financial institutions all around the world, there are investors and executives that are bullish on the future prospects of bitcoin, and hold it in their personal accounts. But in many cases, they can’t express that view in their job. If they manage a stock or bond portfolio, for example, they’ve historically had limited options to express a bullish view on bitcoin. But when a cashflow positive company puts some of its retained earnings into bitcoin, or issues shares to buy bitcoin, or issues convertible notes to buy bitcoin, that can really catch the attention of certain stock and bond managers, and in a security package that they can invest in. They can put a little slice into their portfolio toward a security that is likely to beat their benchmark. The reason that companies like MicroStrategy and Metaplanet tend to trade above their net asset value is because there’s a lot of structural demand for the type of capital they are selling.

There’s still a lot more space for companies to adopt that type of strategy, and in every major currency. Leaders will lead, and followers will follow. They can go the simple route of putting some of their retained earnings into bitcoin, or they can go the higher-conviction and opportunistic route of issuing bitcoin-related equity and debt to their capital providers in order to grow their war-chest faster.

Forward-thinking companies that find themselves in stagnant industries basically have this extra lever to pull: their balance sheet and access to capital markets. There might not be much they can do about their income statement, but by making use of the balance sheet in more innovative ways, they can get a big leg up over their competition, and actually transform their company during a window that may never repeat again.

This continues to make me long-term bullish on bitcoin itself, as well as making me interested in companies that integrate it in some meaningful way on their balance sheet, as long as they do so with proper risk controls.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.